Introduction

In this article, we discuss the power of compounding returns over time to help you understand what the right retirement age could be for you. We’ve also charted some models to help you visualize these ideas below. Some topics we’ll discuss are the following:

- The relationship between annual growth rates, investment multiple, and time.

- How generating higher returns enables individuals to enjoy their lifestyle through investment returns instead of a constant, recurring focus on saving.

- The power of compounding returns and how seemingly trivial differences in returns can have non-trivial implications in building wealth.

- The outcomes associated with managing investment losses.

- Benefits of investing in high-growth innovative companies.

Before we get started, we would like to define 2 key terms:

- Annual Growth Rate: How much your investment grows per year. For example, a $1,000 initial investment growing at 20% annually will be worth $1,200 in 1 year. In year 2, the investment will be worth $1,200 + 20%*($1,200) = $$1,440.

- Investment Multiple: The factor by which your initial investment grew. For example, if a $1 investment becomes $2.50, then your Investment Multiple is 2.5x.

Annual Growth Rates

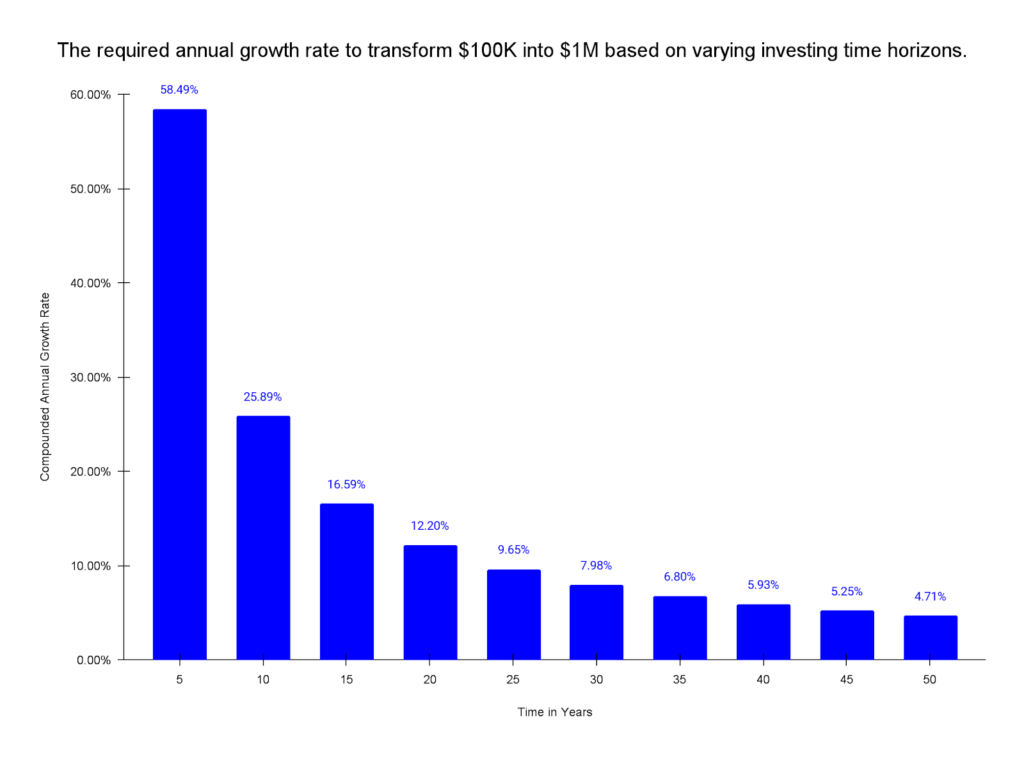

The faster you want to 10x your investment, the higher your annual growth rate must be. The longer your investing time horizon is, the lower the annual growth rate can be. For example, while a 10x in 10 years requires a ~26% annual growth rate, a 10x in 40 years requires a ~6% annual growth rate.

In the chart below, one can see how much the annual growth rate must be to 10x an investment over a certain time period. If one knows how much is needed to retire and the target number of years to retire, then one can use this chart’s model to estimate the required annual growth rate.

One additional caveat with achieving high annual growth rates is that higher growth rates often correlate with higher volatility, which is something to consider for one’s individual risk profile. There can be times of large drawdowns and sour performance when volatility is high.

Saving for Retirement

A popular question asked by many is “How much should I save every year to retire?”. The answer to that depends on the following:

- Time horizon

- Annual growth rate

- Desired amount at retirement

- Current life expenses

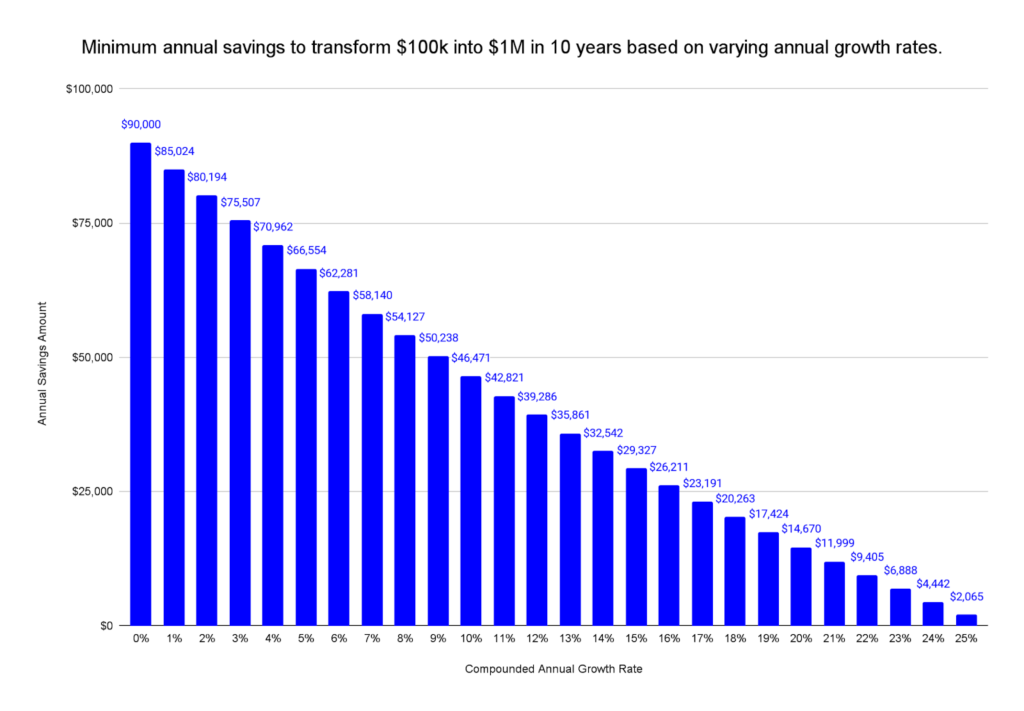

Assuming an individual lives a frugal life and is able to save any dollar amount, the chart below shows how much is needed to save additionally every year for 10 years, given a certain annual growth rate in order to turn $100K into $1M.

Here are some additional insights from the chart above:

- Higher returns allow individuals to enjoy a lifestyle, spend more, and save less.

- In contrast, low returns lead to a necessity for higher savings (implying less consumption and spending) in order to achieve a desired future financial outcome.

- If an individual desires to accumulate $1 million in 10 years with ongoing savings contributions and an initial $100K investment amount, a higher annual growth rate leads to lower required annual savings. For example, a 2% annual growth rate would require ~$80K per year in annual savings, while a 25% annual growth rate would lead to only an implied savings need of ~$2K per year (excluding taxes, fees, etc.) to achieve this specific goal.

Investment Multiple

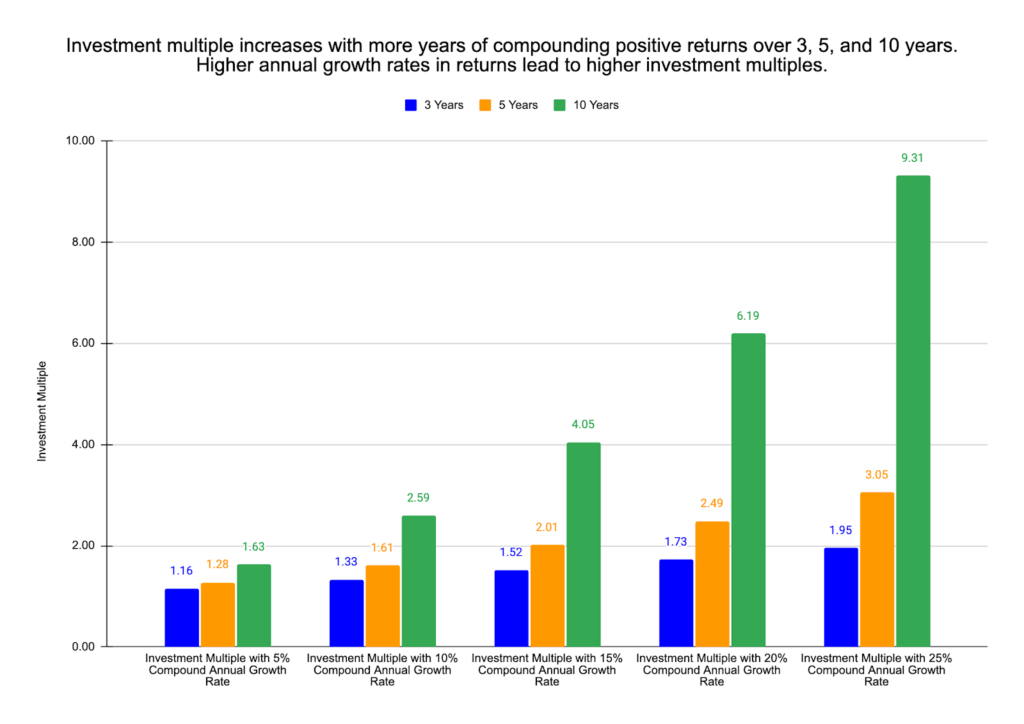

Larger compounding positive returns lead to larger outcomes. For example, if an investor had a 25% annual growth rate, that implies a 2x in 3 years, 3x in 5 years, or a 9x in 10 years. To understand the relationship between how annual growth rates and time horizons impact investment multiples, please see the chart below.

3 insights from the above chart:

- Positive compounding of returns is a beautiful thing. Higher positive annual returns over longer investing time periods lead to higher investment multiples. Small improvements in investment returns over long time periods can lead to significantly higher long-term returns.

- Exponential growth in returns is more apparent in higher annual growth rates. A 25% annual growth rate over 10 years turns $100K into ~$931K, but a 5% annual growth rate over 10 years turns $100K into only ~$163K.

- A higher annual growth rate leads an investor to earn a higher investment multiple in fewer years. For example: a 25% annual return over 3 years has a higher monetary outcome than a 5% annual over 10 years.

Recovering from Losses

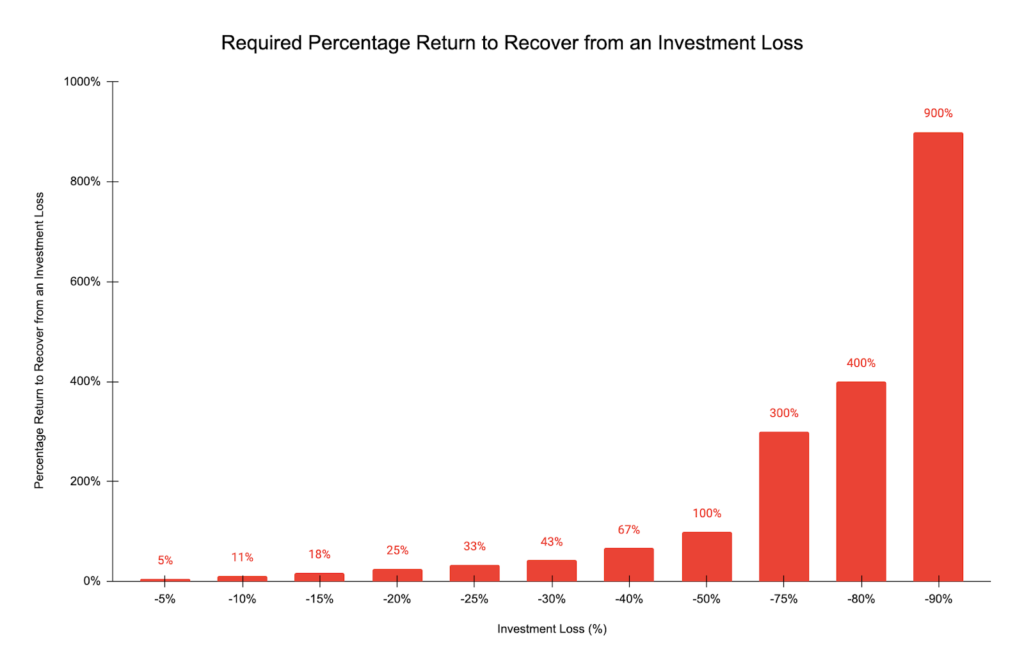

When saving for retirement, one must be cognizant of market fluctuations. Every so often, a recession or significant market volatility occurs, in which investment returns can turn negative. There can be multiple years of negative returns. This is why it is important to never assume that past performance guarantees future returns. Below, we have charted the growth rates that are needed in order to recover from a certain percent loss. This should help understand that less risk and uncertainty can make more sense for a retirement account compared to a risky and low-returning portfolio.

3 insights from the chart above:

- Of course, while the previous charts present an optimistic view about investing, investment losses can occur, and appropriate risk management of a portfolio is a common trait among many successful investors. After suffering from a numeric investment percentage loss, an investor needs to recover more than the percentage loss number in order to break even.

- To recover from a 10% loss, the investor needs ~11.1% returns to break even.

- To recover from a 50% loss, the investor needs a 100% return to break even.

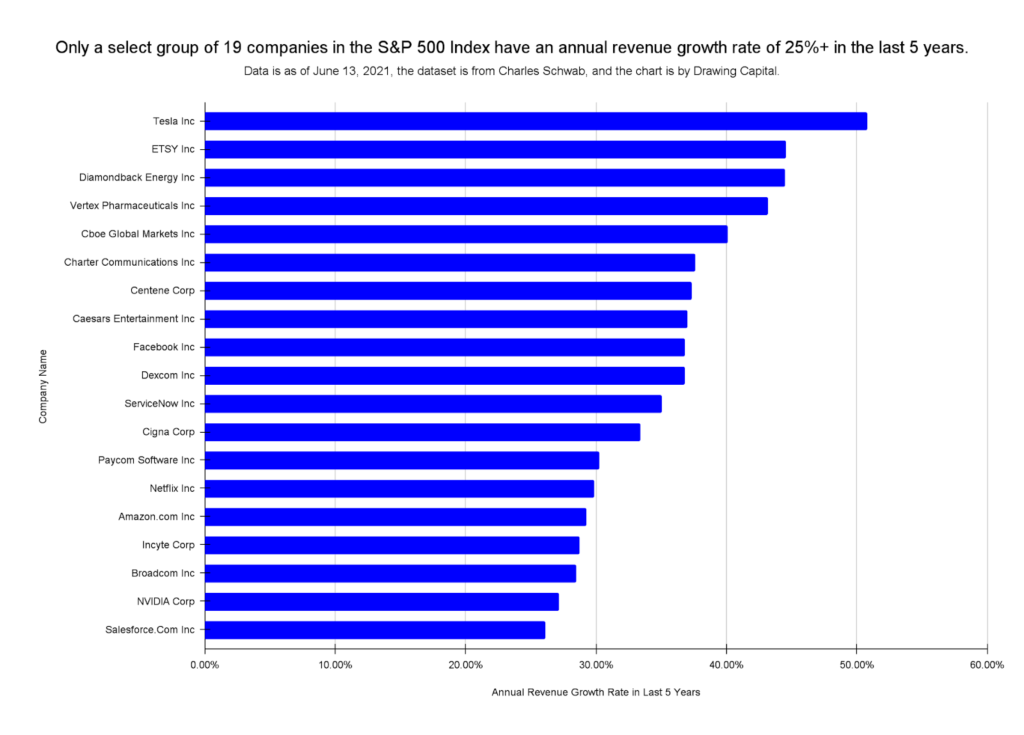

Investing in high-growth, high-margin businesses can be lucrative.

All else equal, companies with higher revenue growth rates and higher margins should command higher EV/sales price multiples because they have greater ability to generate higher and growing cash flows in the future.

In the long term, if people evaluate a business as the present value of discounted future cash flows, then having a higher revenue growth rate allows the business to increase future cash flows due to more future revenue, and higher margins allow the business to convert more of the revenue into cash flow. Hence, when companies both increase margins and increase revenue (especially when they outperform consensus estimates/expectations), this is a “double win” scenario.

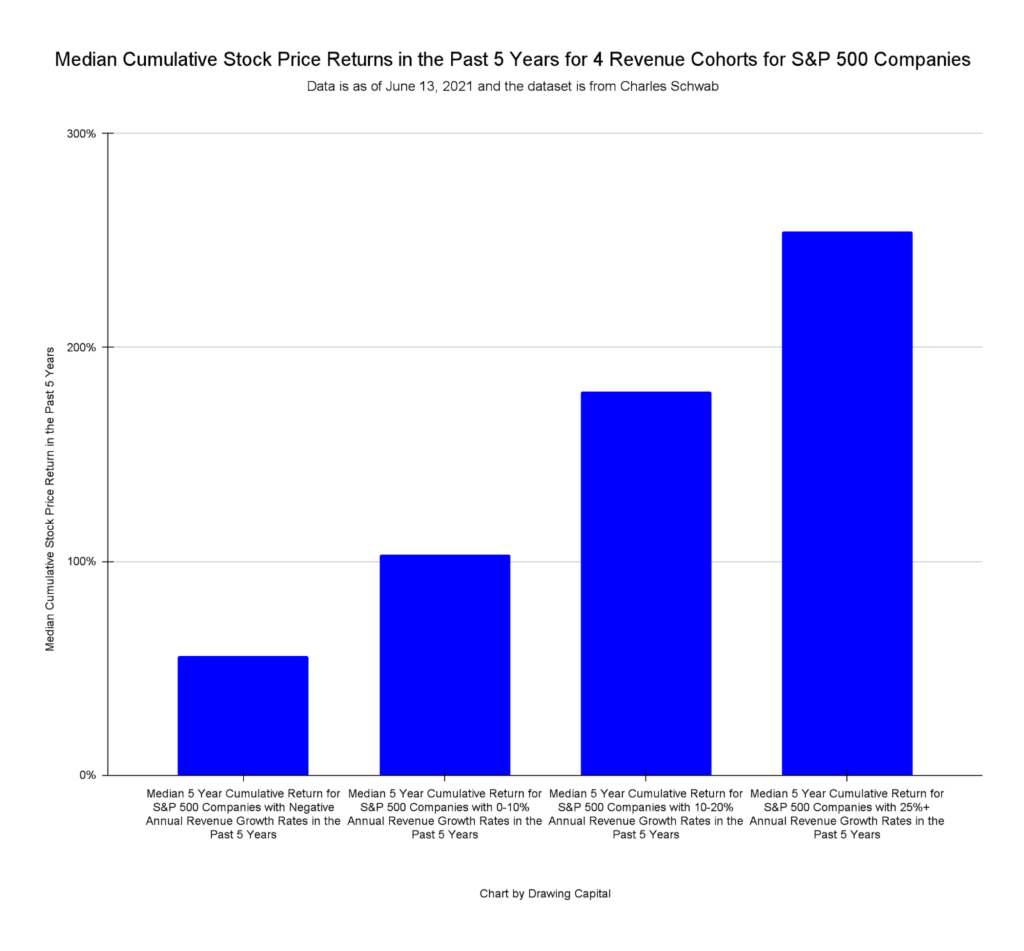

The chart below highlights that on the median over the past 5 years, companies with higher revenue growth rates experienced higher stock price appreciation.

Additionally and as of June 13, 2021, there are only 19 companies in the S&P 500 Index that have experienced 25%+ annual growth rates in their revenues in the past 5 years.

Retiring Early

Given all the discussions above about the importance of longer investment horizons and larger annual growth rates to accumulate more wealth, we want to discuss the positives and downsides of retiring early. Of course, the decision to declare retirement is both a financial decision and a personal decision.

Interestingly, there is a large trend today about “FIRE” or “Financially Independent Retire Early”. This craze, which focuses on financial flexibility and financial freedom, is about being able to stop working around your 30’s or 40’s, but you need sufficient wealth saved up to cover your costs and expenses. Remember, once you retire, you won’t have additional savings accumulating. Your life expenses will eat into your net worth. What you have to do to make sure your assets last is to ensure that your annual growth rate after taxes in dollar terms outpaces your expense rate.

For example, if you are making 15% a year in investments but expense 5% of your wealth on basic needs and lifestyle spending, then this situation creates a sustainable financial situation, provided that the investment returns exceed the spending goals. This is a great position to be in if you can make it last. On the other hand, if you make 5% a year in investments but expense 10%, then you will be losing wealth every year.

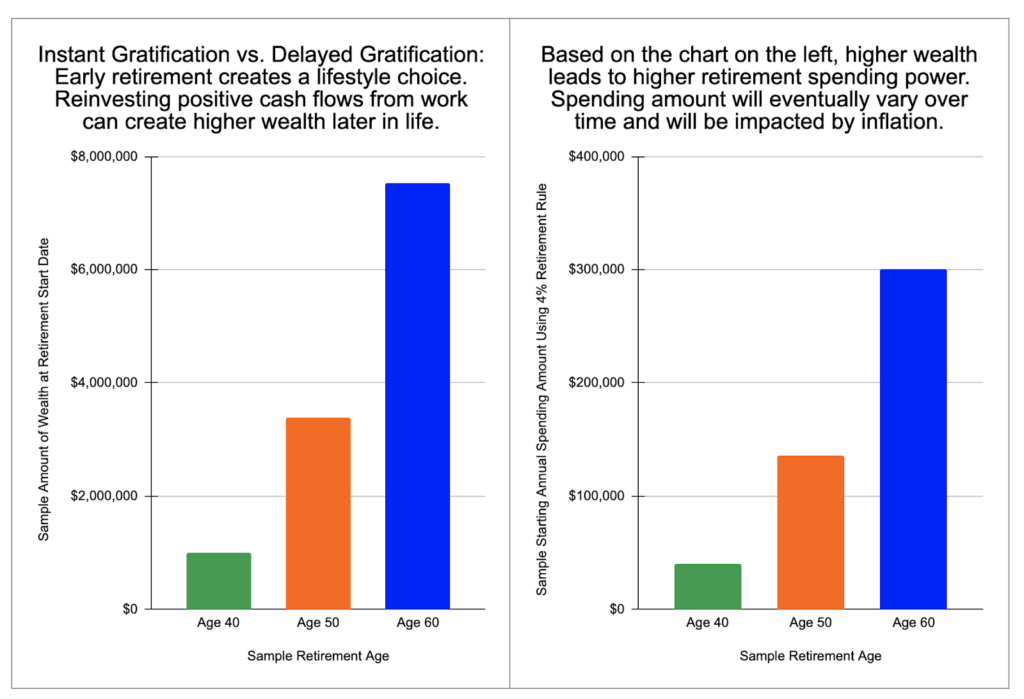

The following illustration highlights a sample scenario with the following assumptions and scenarios, which demonstrates that reinvesting savings and generating positive compounding returns leads to greater wealth accumulation at retirement, which translates into higher spending power and financial freedom during the retirement years:

- Scenario 1: Retire at age 40 with $1 million.

- Scenario 2: Work another 10 years after age 40, retire at age 50, and reinvest both the $1 million and $50K in annual savings at a 10% annual growth rate.

- Scenario 3: Work another 20 years after age 40, retire at age 60, and reinvest both the $1 million and $50K in annual savings at a 10% annual growth rate.

Concluding Thoughts

We hope you enjoyed reading this post. In summary, the topics discussed include:

- The relationship between investment multiple and annualized returns is good to understand, both from a knowledge perspective and also from an implementation perspective in matching your investment goals with your return targets. Higher annualized returns combined with longer time periods lead to higher investment multiples.

- Higher returns can enable a higher quality of life. While low returns lead to a necessity for higher savings (implying less consumption and spending) in order to achieve a desired future financial outcome, higher returns allow individuals to enjoy a lifestyle, spend more, and save less.

- Investing in high-growth, high-margin companies with enduring and growing future cash flows has historically been a lucrative endeavor.

- When an investment loss occurs, it is important to rationally understand the math behind the returns that are needed to break even and recoup the loss from an investment.

- The decision to retire early or continue working is both a financial decision and a personal decision. Different choices can lead to different outcomes, and understanding the distribution of outcomes builds financial knowledge.

In conclusion, understanding investment multiples, compounded annual growth rates, historical outcomes, risk mitigation of losses, and general financial knowledge can help more investors get the odds of investing success in their favor.